Getting a construction loan can feel overwhelming, especially with the changing rates in 2025. Understanding how these loans work and what influences their rates is crucial for anyone planning to build a home. This article will help you navigate the different types of construction loans, factors affecting their rates, and strategies for securing the best deal, including insights into state-specific loan rates and common pitfalls to avoid.

Key Takeaways

- Construction Loans are short-term and usually have higher interest rates compared to traditional mortgages.

- There are various types of construction loans: Construction-to-Permanent, Stand-Alone, and Owner-Builder loans.

- Factors such as economic indicators, credit score, and loan amount impact construction loan rates in 2025.

- Improving your credit score and shopping around for lenders can help secure better loan rates.

- Common pitfalls include underestimating costs and not preparing for rate fluctuations.

Understanding the Basics of Construction Loan Rates

What Are Construction Loans?

Construction loans are short-term financial products designed for the construction phase of a property. Unlike traditional mortgages, these loans typically range between 6.25% and 9.75% APR as of April 2025, depending on lender, location, and creditworthiness.The higher rates are due to the increased risk for lenders, as there is no physical property to use as collateral during the building phase.

How Do Construction Loan Rates Differ from Mortgage Rates?

Construction loan rates are generally higher than mortgage rates due to the uncertainty and risk associated with construction projects. While construction loans are short-term (usually 12 to 18 months) and reflect potential delays or cost overruns, traditional mortgages are long-term with lower, more stable rates.

Types of Construction Loans Available in 2025

Construction-to-Permanent Loans

These loans start as a construction loan and convert to a permanent mortgage once the building is complete. This option simplifies the financing process by combining two loans into one, reducing the need for multiple closings and additional fees.

Stand-Alone Construction Loans

Stand-alone construction loans are separate from your eventual mortgage. You get a loan for construction, and once the home is built, you secure a mortgage to pay off the construction loan. This can be advantageous if you have significant cash reserves but may result in higher overall costs due to two separate loan processes.

Owner-Builder Construction Loans

Owner-builder loans are for those who act as their own general contractor. These loans can be harder to qualify for because lenders see more risk when the borrower is not a professional builder. However, they can save you money if you have the expertise to manage the construction yourself.

Key Factors Affecting Construction Loan Rates in 2025

Economic Indicators

The broader economic environment significantly impacts construction loan rates. A strong economy may lead to higher rates to control inflation, while a weaker economy might result in lower rates to encourage borrowing. Keeping track of central bank policies and economic trends can help anticipate rate changes.

Credit Score and Financial History

Your credit score and financial stability are crucial for securing favorable loan rates. Lenders typically look for a credit score of 620 as a minimum, but a score of 740 or higher is ideal for the best rates. A strong financial track record can improve your creditworthiness and lower your interest rates.

Loan Amount and Duration

Larger loan amounts and longer durations can lead to higher rates due to increased risk for lenders. Balancing your loan needs with what you can afford to repay over time is essential for managing costs.

How to Qualify for a Construction Loan

- Credit report

- Builder license and insurance proof

- Timeline for construction phases

- Land ownership documents

Credit Requirements

Lenders generally require a credit score of at least 620 for a construction loan. To secure the best rates, aim for a score of 740 or higher, demonstrating reliability and financial stability.

Necessary Documentation

When applying for a construction loan, you’ll need:

- Detailed construction plans

- A signed contract with a licensed builder

- A comprehensive budget

- Financial documents like tax returns, W-2s, and bank statements

Having these documents ready can expedite the approval process.

Construction Loan Rate Trends Forecast (2025–2026):

Experts anticipate construction loan rates to stabilize in late 2025 as inflation cools and supply chain disruptions ease. Expect rates to slowly trend downward into early 2026.

Choosing the Right Lender

Not all lenders offer construction loans. Banks are more likely to provide these loans compared to credit unions or online lenders. Some banks may offer special rates for existing customers, so shopping around is crucial.

Strategies for Securing the Best Construction Loan Rates

Improving Your Credit Score

Boosting your credit score can have a major effect on the interest rate you receive. To enhance your score, focus on settling any existing debts, steer clear of opening new credit accounts, and make sure you pay your bills on time.

Shopping Around for Lenders

Explore various lenders to find the best rates. Banks, credit unions, and online lenders offer different terms, so it’s beneficial to compare options. Starting with banks, especially if you have existing accounts with them, might give you access to special rates.

Negotiating Loan Terms

Once you have multiple offers, don’t hesitate to negotiate. You can request lower interest rates, reduced fees, or more favorable repayment terms to get better loan conditions.

Impact of Inflation and Interest Rates on Construction Loans

Inflation Trends

Inflation plays a critical role in shaping construction loan rates. When inflation is high, the cost of materials and labor rises, leading to increased construction expenses. Lenders respond to this by raising interest rates to protect their margins and offset the higher costs associated with borrowing. As of 2025, inflationary pressures have been a significant factor in the construction loan market, leading to higher rates compared to previous years.

For prospective borrowers, it’s essential to monitor inflation trends closely. When inflation rates are high, construction loan rates are likely to be elevated. Keeping an eye on economic reports and forecasts can help you anticipate rate changes and plan accordingly. If inflation shows signs of stabilizing or decreasing, you might see a corresponding dip in construction loan rates, presenting an opportunity to secure better financing terms.

Federal Reserve Policies

The Federal Reserve‘s monetary policies directly influence construction loan rates. The Fed adjusts interest rates to control inflation and stabilize the economy. When the Fed raises rates to combat inflation, construction loan rates typically follow suit, becoming more expensive. Conversely, when the Fed lowers rates to stimulate economic growth, borrowing costs generally decrease.

In 2025, the Fed’s stance on interest rates will be pivotal for construction loan rates. As of Q1 2025, the Federal Reserve has maintained interest rates at 5.25%, citing persistent core inflation and cautious optimism in labor market resilience. Recent policy shifts, including adjustments to the federal funds rate, can create fluctuations in borrowing costs. Borrowers should stay informed about Fed meetings and policy announcements, as these can provide insights into future rate trends. Understanding the Fed’s monetary policy can help you make more informed decisions about timing your loan application and locking in rates.

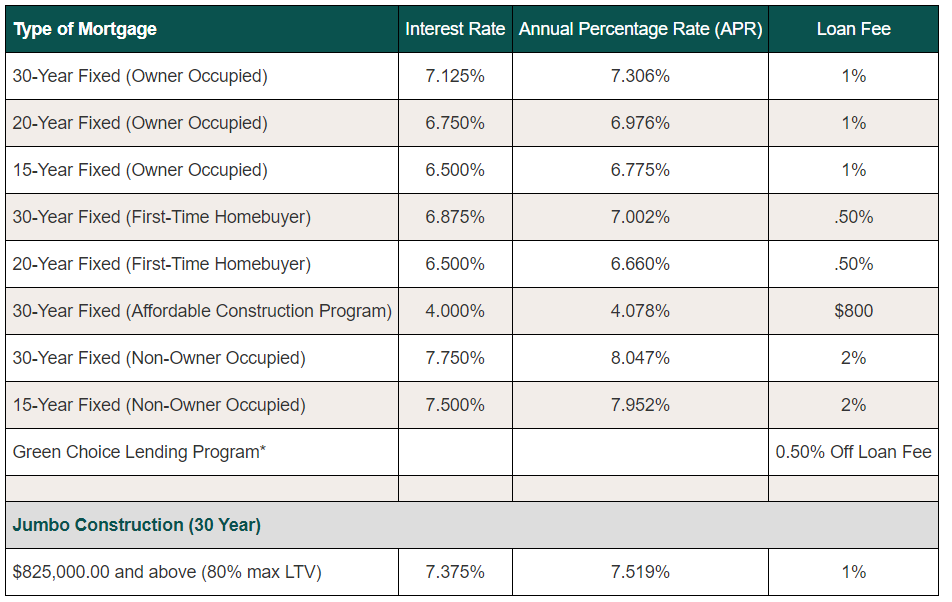

To give you a clearer picture of current rates, here’s a table outlining the mortgage and construction loan rates available in 2025, including specific programs and options that may be relevant to your financial planning.

Long-Term Financial Planning for Construction Loans

Budgeting for Future Expenses

Effective long-term financial planning is crucial when taking out a construction loan. Once your construction project is completed and the loan transitions into a permanent mortgage, your financial obligations will shift. It’s important to budget for these future expenses to avoid financial strain.

Start by estimating the potential mortgage payments you’ll face after the construction loan ends. Consider using online mortgage calculators to simulate different scenarios based on various interest rates and loan terms. Additionally, plan for maintenance and unexpected costs that might arise once you move into your new home. By preparing for these future expenses, you can ensure a smoother financial transition and avoid surprises.

Managing Debt-to-Income Ratio

Maintaining a balanced debt-to-income (DTI) ratio is crucial for your long-term financial health. This ratio evaluates how your monthly debt payments compare to your income. A high DTI can make it harder to obtain new loans and create financial strain.

To keep your DTI ratio in a healthy range, strive to keep your debt payments at a manageable level. Once you’ve obtained a construction loan, concentrate on reducing any existing debts and refrain from accumulating new ones. If feasible, seek opportunities to boost your income through extra work or investments to strengthen your financial position. Regularly monitor and adjust your DTI ratio to ensure continued financial stability both during and after your construction project.

States with the Best Construction Loan Rates in 2025

Construction loan rates can vary widely across the U.S., but for homebuyers in the Pacific Northwest, Washington and Oregon are currently two of the most borrower-friendly states. Thanks to steady housing demand, active lending markets, and support for sustainable development, these states offer some of the most competitive options in 2025 for those looking to build.

Washington

Overview:

Washington’s construction loan market remains strong, especially in high-growth cities like Seattle, Spokane, and Tacoma. The state’s booming tech industry, expanding infrastructure, and steady population growth have all contributed to a healthy appetite for new housing. This ongoing demand encourages more lenders to offer competitive products—particularly construction-to-permanent loans that simplify the building process.

Why it’s Competitive:

Local banks, credit unions, and national lenders operating in Washington often provide flexible financing options tailored for the state’s unique market. Many offer interest-only payments during the build phase, and some waive origination fees for qualified applicants. For borrowers with good credit and a solid plan, rates may start as low as 6.375% APR, though exact numbers will vary by project size, location, and borrower profile.

Pro Tip:

If your build includes energy-efficient features or follows green building standards, some Washington-based lenders offer rate reductions or closing cost credits. Look into local programs promoting sustainable housing—they may make your project more affordable.

Oregon

Overview:

Oregon’s real estate market continues to grow steadily, with strong construction activity in cities like Portland, Eugene, Salem, and Bend. Whether you’re planning an urban infill project or a rural home build, Oregon offers a balanced mix of lender options, land availability, and state-level incentives for residential development. Local governments have also streamlined permitting in some regions to encourage responsible growth.

Why it’s Competitive:

Construction loan rates in Oregon typically range from 6.5% to 7.25% APR, depending on the borrower’s credit, builder credentials, and loan structure. Credit unions and community banks often lead with more personalized service and fewer hidden fees than larger institutions. Many lenders offer one-time close construction-to-perm loans that convert to a standard mortgage after completion—saving time and money.

Pro Tip:

If you’re building outside Portland or other urban centers, smaller lenders may be more open to customized terms, including lower down payments, flexible draw schedules, and manual underwriting for self-employed borrowers. It’s worth checking in with local financial institutions that understand the specific challenges of building in rural or semi-rural areas.

Note: The Consumer Financial Protection Bureau (CFPB) advises that obtaining multiple Loan Estimates from different lenders can lead to significant savings. By comparing these estimates, homebuyers can potentially save between $600 and $1,200 annually. This process allows you to assess various loan terms, interest rates, and fees, ensuring you select the mortgage that best fits your financial situation.

Additionally, Bankrate recommends comparing offers from at least three lenders. This approach not only helps in uncovering the most favorable loan terms but also provides leverage to negotiate better rates and fees. It’s important to keep these pre approval requests within a 45-day window to minimize any impact on your credit score.

By shopping around and getting pre-qualified with multiple lenders, you enhance your chances of securing the most advantageous construction loan rates and terms available.

Common Pitfalls to Avoid with Construction Loans

Underestimating Costs

Underestimating construction costs is a common mistake. Ensure you have a detailed budget that includes all potential expenses, and add a buffer for unexpected costs.

Ignoring Loan Terms

Understanding the specific terms of your construction loan is crucial. Be aware of interest rates, repayment schedules, and any penalties for late payments to avoid financial strain.

Not Preparing for Rate Fluctuations

Construction loans often come with variable interest rates. Prepare for potential rate increases to avoid higher monthly payments than expected. Consider locking in a rate or having a plan to manage rate changes.

Need expert help navigating 2025’s construction loan market? Get a personalized rate estimate today and start your build with confidence.

Conclusion

In 2025, understanding construction loan rates is essential for anyone looking to build a home. These loans differ from traditional mortgages and come with their own set of rules and higher interest rates. By knowing the basics, understanding what lenders look for, and employing strategies to secure the best rates, you can make informed decisions. Keep an eye on market trends, consult with experts, and choose the right lender to turn your dream home into a reality without financial surprises.